Mag 7 led selloff in Q1, as Large Caps, Mid Caps, and Small Caps fell into correction

Last week, we wrote about how tariffs and policy uncertainty were weighing on small business and consumer sentiment, contributing to the recent selloff in markets.

Since then, we’ve learned that:

- The reciprocal tariffs planned for April 2 are now likely to be more targeted than previously expected

- Consumer Expectations fell to a 12-year low today, as they worried about tariffs and the stock market

And it’s no wonder consumers are worried about the stock market. Since peaking in mid-February, we saw Large Caps, Mid Caps, and Small Caps all fall into correction (down 10+%) by mid-March (chart below, red line), leading to (premature) talk of recession.

The selloff actually hit the Mag 7 the hardest (purple line).

At their lows, the Mag 7 was down 15%, but the rest of the Nasdaq-100® was “only” down 12% (lighter blue line) and the rest of the S&P 500 was down just 8% (orange line).

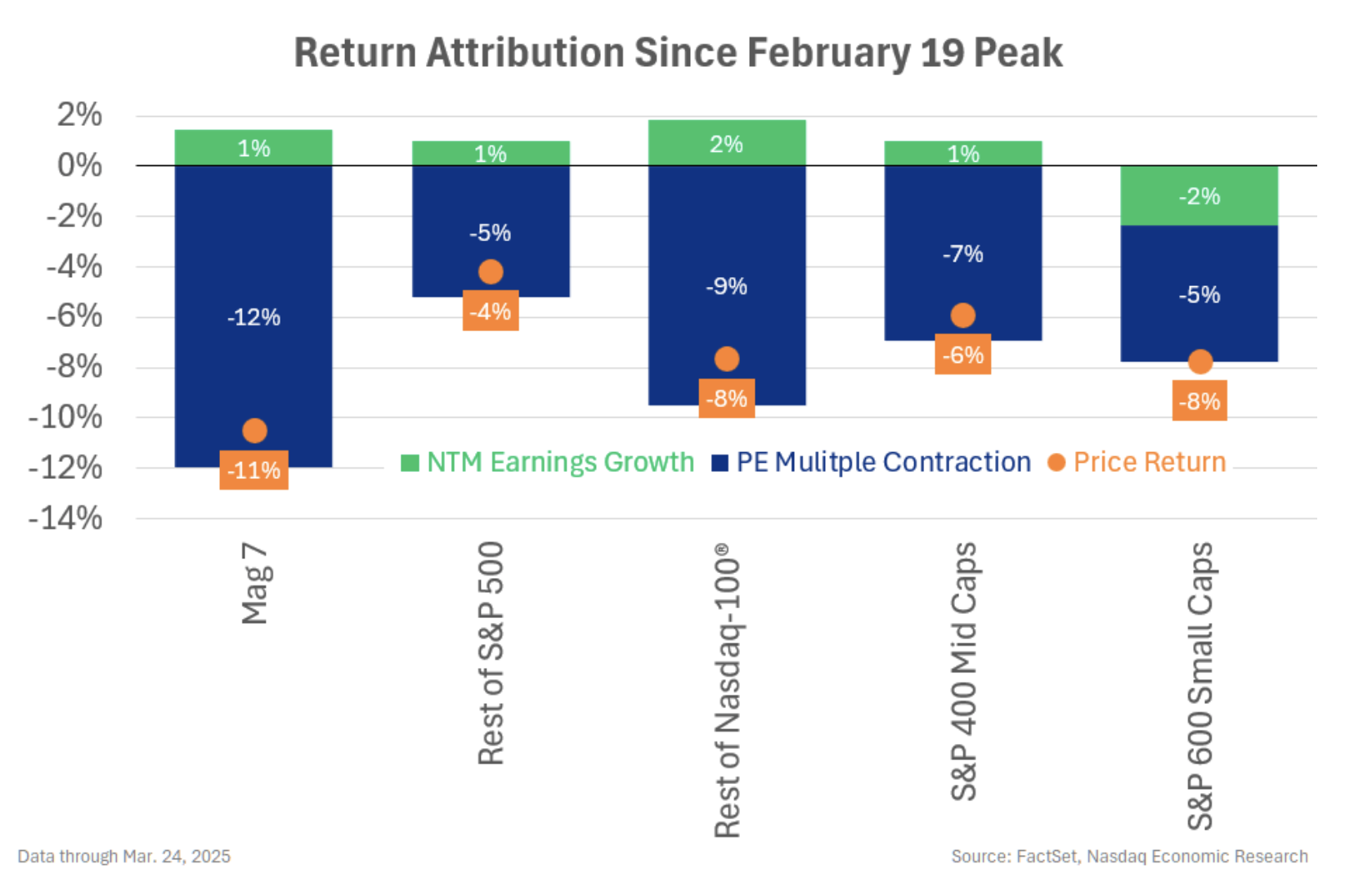

Correction entirely attributable to falling valuations as earnings are up since market peak

If we look at the drivers of the selloff, it’s no surprise the Mag 7 was hit the hardest.

That’s because the selloff has been driven by falling PE multiples (chart below, blue bars), as investors aren’t willing to pay as much for future earnings.

While US PE multiples were near historic highs prior to the selloff, indicating US stocks were “priced for perfection,” they were higher still for the Mag 7.

So those valuations became harder to maintain as they’ve faced headwinds from multiple factors (tariffs, uncertainty, slower economic growth…), and they’ve now fallen to less stretched (but still relatively high) levels.

For the Mag 7, add AIcompetition to the list of headwinds (and other idiosyncratic factors), and their forward PEs are down 12% in just five weeks.

However, the selloff has not been driven by fundamentals.

In fact, across the board for Large Caps and Mid Caps, forward earnings are up (slightly) since the market peaked (green bars), in another sign that recession risk remains low so far. (Only Small Caps have seen their earnings shrink.)

Analysts suggesting worst of selloff may be over

For now, with earnings holding up, it looks like this selloff has been the market correcting for slower growth and greater uncertainty – not recession. And some analysts are now suggesting the worst of the selloff is over.

With the Nasdaq-100 up +5% and the S&P 500 up +4% from their mid-March lows, they may be right. We’ll see.

The information contained above is provided for informational and educational purposes only, and nothing contained herein should be construed as investment advice, either on behalf of a particular security or an overall investment strategy. Neither Nasdaq, Inc. nor any of its affiliates makes any recommendation to buy or sell any security or any representation about the financial condition of any company. Statements regarding Nasdaq-listed companies or Nasdaq proprietary indexes are not guarantees of future performance. Actual results may differ materially from those expressed or implied. Past performance is not indicative of future results. Investors should undertake their own due diligence and carefully evaluate companies before investing. ADVICE FROM A SECURITIES PROFESSIONAL IS STRONGLY ADVISED. © 2025. Nasdaq, Inc. All Rights Reserved.